Table of Content

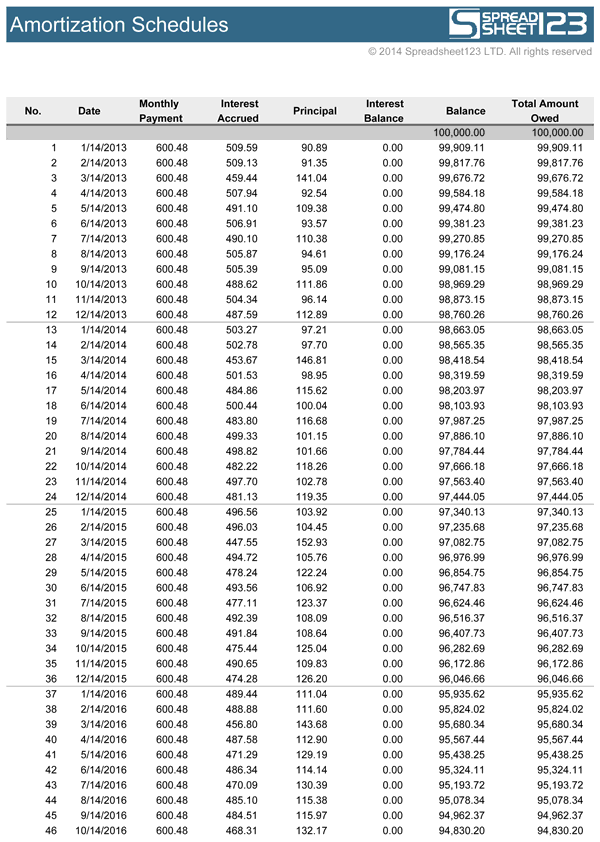

The earlier a borrower makes prepayments, the more it reduces the overall interest paid, typically leading to quicker mortgage repayment. The amortization table below illustrates this process, calculating the fixed monthly payback amount and providing an annual or monthly amortization schedule of the loan. For example, a bank would amortize a five-year, $20,000 loan at a 5% interest rate into payments of $377.42 per month for five years. The Mortgage Amortization Calculator provides an annual or monthly amortization schedule of a mortgage loan.

At the beginning of a mortgage term, most of the payment goes for interest and little is going towards paying down the principal. Each month the principal and interest payment is recalculated. The interest payment is calculated based on the remaining balance of the loan, the lower the balance, the less interest payment the borrower has to pay for that month. That means as time passes, the monthly payments will shift more towards the principal than the interest. Eventually, the mortgage is paid off in full when the balance reaches $0. To learn more about amortization schedules and how to create one, visit the amortization schedule calculator.

Explore personal banking

Annual tax amount is calculated and then divided by the number of payments per year. Usually, the interest rate that you enter into an amortization calculator is the nominal annual rate. However, when creating an amortization schedule, it is the interest rate per period that you use in the calculations, labeled rate per period in the above spreadsheet.

Nonetheless, our mortgage amortization calculator is specially designed for home mortgage loans. Certain businesses sometimes purchase expensive items that are used for long periods of time that are classified as investments. Items that are commonly amortized for the purpose of spreading costs include machinery, buildings, and equipment. From an accounting perspective, a sudden purchase of an expensive factory during a quarterly period can skew the financials, so its value is amortized over the expected life of the factory instead. Although it can technically be considered amortizing, this is usually referred to as the depreciation expense of an asset amortized over its expected lifetime.

How we make money

Some people struggle with discipline, while others prefer a fixed routine. One person might find it easier to automatically pay a bit more each month, while another might get a sense of accomplishment by making a larger payment at once. At the end of the day, you should choose the method that helps you keep paying extra. Automated habits routinely beat out our best stated intentions.

Use this amortization calculator to help you determine how many months it could take to pay off your loan with or without making extra payments. Extra payment amortization schedule can certainly help you get out of your debt faster. You can make one-time, one-time yearly or for each payment extra payments towards the principal and therefore shorten original mortgage term. Every additional payment to required mortgage payment scheme is a step towards a life without debt.

AMORTIZATION WITH EXTRA PAYMENTS

There are some important uses for the shifting cell reference, such as when calculating remaining balance. You want it to use the formula from the previous row, and you want that to keep shifting as it goes down. Instead of building formulas or performing intricate multi-step operations, start the add-in and have any text manipulation accomplished with a mouse click. Please pay attention, that we use absolute cell references because this formula should copy to the below cells without any changes. How much principal and interest are paid in any particular payment.

You decide to start making extra payments on the third year of your loan. The following chart estimates how much you’ll save if you pay an extra $50, $100, or $200 per month. Furthermore, you’ll save considerably more on interest charges the earlier you make extra payments. Based on our example, you’ll save $23,648.44 on total interest if you make extra payments at the start of your mortgage. Meanwhile, you’ll save $15,618.66 on total interest if you make additional payments on the 6th year. That’s money that can go to your emergency savings, home repairs, or retirement funds.

A mortgage loan is typically a self-amortizing loan, which means both principal and interest will be fully paid off when you make the last payment on the predetermined schedule — usually monthly. Our mortgage amortization table shows amortization by month and year. Making extra mortgage payments are a good way to reduce your interest charges and shorten your term. It’s a viable option if you have extra income but cannot afford to refinance to a shorter term. But before you make additional mortgage payments, make sure to ask your lender about prepayment penalty. Paying expensive penalty fees defeats the purpose of gaining savings on extra payments.

You should not forget that required mortgage monthly payments include not only principal payment but also a great amount of interest payment. That means high additional costs for you and more money for your bank. An amortization schedule shows more than how much of your monthly payment will go towards paying down your principal. If you scroll down to the bottom of the page, you’ll also see exactly how much you’ll pay in interest over the life of the loan. In the case of your dream $60,000 vehicle, it’s just shy of a whopping $20,000.

This is better than having it stretched out at $100 per month. If you have $200 saved up today and can save $100 a month, it wouldn’t make sense to wait 10 months to add $1,200 to a mortgage payment. Again, you’re better off paying whatever extra amount you have now. In general, the sooner you make extra payments the more money you will save.

But if you run the numbers with a rental cash flow calculator and find you can still end up in the black each month, it can save you a ton on interest in the long term. Most homeowners normally make monthly mortgage payments, which is equivalent to 12 payments annually. To pay extra on your mortgage, you can make an additional 13th payment. To make it easier, you can time this when you get large work bonuses or tax returns within the year. It’s a good way to use extra funds instead of completely splurging on other expenses. You can make your 13th payment at the beginning of the year or towards the end of the year.

No comments:

Post a Comment